Financial Advisor Resources

Featured post

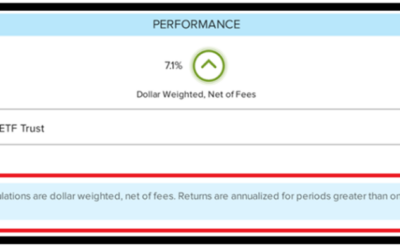

Annualized vs. Cumulative Performance Reports for RIAs

Many Registered Investment Advisors (RIAs) face challenges in accurately reporting investment performance to clients, particularly in differentiating between annualized and cumulative returns. Misunderstandings lead to client confusion, increased risk, misplaced expectations, and potential dissatisfaction with investment strategies. CircleBlack’s...

Blog

Annualized vs. Cumulative Performance Reports for RIAs

Many Registered Investment Advisors (RIAs) face challenges in accurately reporting investment...

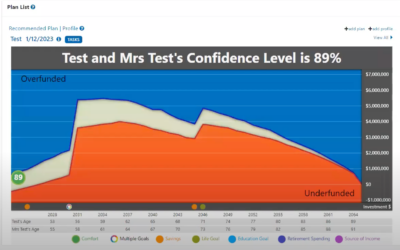

Best Tools for Educating Clients on Financial Topics

Wealth advisors navigate complex waters, often grappling with the dual tasks of managing intricate...

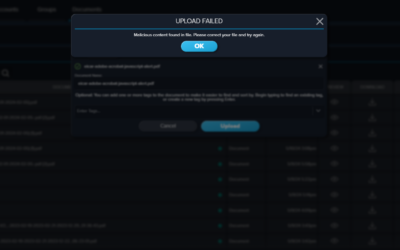

Improving Cybersecurity at RIA Firms

Financial advisors face numerous challenges in managing and sharing sensitive client documents....

Customer Stories

How San Blas Securities Delivers Caring and Approachable Service

“With CircleBlack, it’s relatively seamless to transition between screens, making it easy for clients and advisors to get on the same page.”

See how CircleBlack supports client service at San Blas Securities.

Rovin Capital Improves Client Relationships with CircleBlack

“The platform provides everything we need and is very user-friendly. The process for integrating our existing technology stack was seamless.”

See how CircleBlack serves as a mission critical app for ops at Glen Eagle.

Diversified Capital Group Offers Seamless Client Portal

“CircleBlack has become the nucleus for our fintech allowing us to aggregate everything into one dashboard.”

See how CircleBlack’s client portal provide seamless portfolio management.

Guides

Guide to CircleBlack’s Integration Ecosystem

CircleBlack, the all-in-one with choice wealth management platform, has a broad set of wealthtech...

Prospecting, Acquisition, and Beyond: A Guide to Growing Your Client Base

In the ever-evolving financial advisory world, one essential skill sets the stage for success:...

Guide to Tax Planning

Financial advisors constantly seek ways to increase value, create personalized solutions, and...

Press

CircleBlack Names Robert Keller as Chief Product Officer

Accomplished investment technology strategist to head product management for CircleBlack’s “all-in-one, with choice” platform.

TradePMR Launches a New Integration with CircleBlack Designed to Streamline Connectivity with the Wealth Management Platform

CircleBlack, an all-in-one platform for relationship-focused advisors, and TradePMR, a technology and custodial services provider, announced today a new integration.

CircleBlack Appoints Robert Baxter as Chief Technology Officer

Veteran wealthtech executive to head technology development and operations as the organization continues to scale and deliver best-in-class solutions for client-centric financial advisors.

See CircleBlack in action

Our all-in-one wealth management platform streamlines operations, reporting, and client engagement for your RIA firm.